Every small business borrows money at times. Most small businesses borrow money to buy a fixed asset. It is a long-term obligation to borrow the amount. Recording and processing loan payments takes several steps. Depending on the type of loan, you'll need a suspense account. This account holds value that is awaiting a future transaction. See the following examples for more information. You can use suspense to account for various transactions.

Bookkeeping account knowledge: Tax knowledge

The state of tax education is different in New Zealand than other countries. Few comparative studies have been undertaken and little information is available about New Zealand's initial tax courses. This knowledge gap was filled by the present study. This study determined what students needed to know to successfully perform their bookkeeping and accounting duties. This study also aimed to determine whether practitioners' expectations of students' tax knowledge are met.

A tax accounting course is one way to increase your tax knowledge. This course is usually completed in a week. It reinforces the information you have received from previous classes. This course is great for students, managers, or business owners who want to learn more about taxation. Taxation is always changing so you will need to keep up-to-date with the latest developments. You can maintain the high quality service you provide to your clients by continuing your education.

Classification of bookkeeping account

The basic structure of a company's books is based on the classification of its bookkeeping accounts. There are three types of accounts: nominal, balance sheet, income, and expense. Because they are the income and expense accounts of a business, nominal accounts are the most common. Because they don't close at the end, but carry forward to the next accounting period, they are also known as real accounts. Income statement accounts are used to prepare financial statements such as profit and loss accounts.

First, you need to create a chart. A chart of accounts is a listing of all accounts used by a company. Each account is categorized according to its purpose. These accounts can be classified according to their size, which depends on how large the business is. They can be divided into four main categories: expense, liability, equity and asset. Some journals can be divided according to their purpose. Assets and expenses are classified under one category.

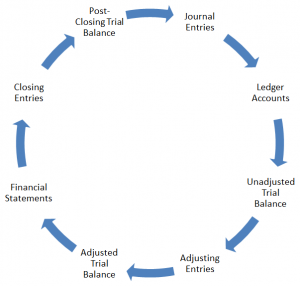

Recording transactions

The recording of transactions is crucial in accounting. Financial statements that are inaccurate could be caused by mistakes in the recording process. Accounting professionals must understand the purpose of recording. To analyze transactions, the recording is necessary. These transactions are analysed using the accounting equation. We will discuss the purpose of recording in this article. These are just a few examples.

First, determine the transactions that need to be recorded. These transactions may include sales orders, bills and cash register tapes. These records are then kept in journals, ledgers, or trial balances. Small businesses might use a simple cash register. After the records have been recorded, financial statements can be created by combining the data. Some businesses might choose to record transactions in other journals.

Trial balance

What is a trial account balance? Simply put, a trial balance is a list of the nominal ledger accounts. Each account in the list contains a debit or credit balance. Also, the name and number of the nominal ledger accounts are listed on the trial balanced. Click the link below to view a trial balance.

You can check the trial balance to see if your bookkeeping accounts are in error. You should aim for a trial balance to be at zero. However, mistakes can cause it not being zero. You may have entered incorrect amounts or transposed a column to create a non-zero trial account. You can find out the difference between credit and debit columns to determine the source.

FAQ

Why Is Accounting Useful for Small Business Owners?

Accounting is not only for large businesses. Accounting can also be useful for small businesses because it allows them to track how much money they spend and make.

You likely already know how much money you get each month if your small business is profitable. But what if you don't have an accountant who does this for you? You may be wondering where your money is being spent. You might forget to pay your bills on time which could negatively impact your credit rating.

Accounting software makes managing your finances simple. There are many choices. Some are absolutely free while others may cost hundreds or even thousands of dollars.

It doesn't matter which accounting system you use; you need to know its basic functions. By doing this, you will not waste time learning how to operate it.

These are the basics of what you should do:

-

You can enter transactions into your accounting system.

-

Keep track of your income and expenses.

-

Prepare reports.

These three steps will help you get started with your new accounting system.

What does an accountant do and why is it important?

An accountant keeps track of all the money you earn and spend. An accountant also records how much tax you have to pay and the deductions that are allowed.

Accounting helps you manage your finances by keeping track your income and expenses.

They assist in the preparation of financial reports for both individuals and businesses.

Accountants are necessary because they must be knowledgeable about all things numbers.

Accountants also assist people with filing taxes to ensure that they are paying as little tax possible.

What type of training is required to become a Bookkeeper?

Basic math skills are necessary for bookkeepers. They need to be able to add, subtract, multiply, divide, fractions and percentages.

They must also be able to use a computer.

Most bookkeepers have a high school diploma. Some have even earned college degrees.

What happens if my bank statement isn't reconciled?

You might not realize that you made a mistake in reconciling your bank statements until the end.

At that point, you'll have to go through the entire process again.

Why is reconciliation so important?

It is vital because mistakes can happen at any time. Mistakes include incorrect entries, missing entries, duplicate entries, etc.

These problems can have grave consequences, including incorrect financial statements or missed deadlines, overspending and bankruptcy.

Statistics

- a little over 40% of accountants have earned a bachelor's degree. (yourfreecareertest.com)

- BooksTime makes sure your numbers are 100% accurate (bookstime.com)

- Given that over 40% of people in this career field have earned a bachelor's degree, we're listing a bachelor's degree in accounting as step one so you can be competitive in the job market. (yourfreecareertest.com)

- a little over 40% of accountants have earned a bachelor's degree. (yourfreecareertest.com)

- In fact, a TD Bank survey polled over 500 U.S. small business owners discovered that bookkeeping is their most hated, with the next most hated task falling a whopping 24% behind. (kpmgspark.com)

External Links

How To

How to Become a Accountant

Accounting is the science and art of recording financial transactions and analyzing them. It involves the preparation and maintenance of various reports and statements.

A Certified Public Accountant or CPA is someone who has passed an exam and received a license from the state board.

An Accredited Finance Analyst (AFA), an individual who meets certain requirements established by the American Association of Individual Investors. A minimum of five years investment experience is required to become an AFA by the AAII. A series of exams is required to assess their knowledge of securities analysis and accounting principles.

A Chartered Professional Accountant, also known as a chartered accountant or chartered accountant, a professional accountant who holds a degree from a recognized university. CPAs must comply with the Institute of Chartered Accountants of England & Wales’ (ICAEW) educational standards.

A Certified Management Accountant is a professional accountant who specializes in management accounting. CMAs must pass exams administered annually by the ICAEW. They also need to continue continuing education throughout their careers.

A Certified General Accountant (CGA) member of the American Institute of Certified Public Accountants (AICPA). CGAs must take multiple tests. One of these is the Uniform Certification Examination (UCE).

International Society of Cost Estimators, (ISCES), offers the Certified Information Systems Auditor (CIA), a certification. Candidates for the CIA need to complete three levels in order to be eligible. These include practical training, coursework and a final examination.

An Accredited Corporate Compliance Officer (ACCO) is a designation granted by the ACCO Foundation and the International Organization of Securities Commissions (IOSCO). ACOs need to have a bachelor's degree in finance, public policy, or business administration. They must also pass two written exams as well as one oral exam.

The National Association of State Boards of Accountancy's Certified Fraud Examiner credential (CFE), is awarded by NASBA. Candidates must pass three exams, and get a minimum score 70%.

International Federation of Accountants is accredited a Certified Internal Audior (CIA). Candidates must pass four exams covering topics such as auditing, risk assessment, fraud prevention, ethics, and compliance.

American Academy of Forensic Sciences (AAFS) designates an Associate in Forensic Account (AFE). AFEs must be graduates of an accredited college or university that has a bachelor's in accounting.

What is an auditor? Auditors are professionals who perform audits of financial reporting systems and their internal controls. Audits can either be done randomly or based on complaints about financial statements received by regulators.