There are many choices if you're thinking about a career in accounting. There are many options: working in large organizations, at one of the "Big Four" accounting companies, or starting your own business. Below are the pros, cons and benefits of each path. Which one would suit you best? Which one will have the greatest impact on your salary? Which path will lead you to a higher salary? Which experience are you required to succeed?

One organization.

It might not make sense to work for just one accounting firm if your career goal is to become an accountant. People tend to stay in an entry-level position for one to five years. It all depends on the economy and other opportunities. This article assumes that you will remain at the same company for one year. You will ultimately decide what type of work environment suits you best.

A high salary

If you love to crunch numbers, an accounting career may be right for you. The median annual salary for accounting professionals is $92,246, making it an attractive career choice. You will oversee all aspects of the company's finances as head of an accounting department. These include financial reports, general ledgers and payroll. They also cover accounts payable and receivable as well tax compliance. Additionally, you will be responsible for budgeting and tax compliance.

Some accountants work as partners in small businesses, while others work as CFOs in larger firms. Some work as independent consultants, helping clients with their tax returns. High salaries are available in accounting careers, so it's possible to work remotely. You just need to be creative and determined. But if you're determined, you'll find a high-paying accounting job that doesn't require a big commute or much travel.

Working in an "Big Four” accounting firm

Many people have dreams of working in one of the Big Four accounting companies. But what are the advantages and disadvantages? There are many reasons to consider a Big Four accounting firm if you are looking for an entry-level position in the field of accounting. Here are some pros and cons of working in a Big Four versus a local firm. This will help you decide if this is the right job for you.

When applying to a Big Four firm, be sure to demonstrate the qualities that make a good employee for the company. You should be confident and determined to serve the clients and company. It is important that you can demonstrate your commitment and commercial acumen, as well as emotional intelligence. Additionally to these qualities, you will need strong computer skills as well as a good understanding of accounting and tax law.

Start your own accounting firm

Here are some important considerations when you start an accounting company. Although there are many benefits to starting your own business, it is important to do some research. You must be able to offer legal advice to your clients in order for you start a business legally. This is based on your education and certification. CPAs are the only ones who can file reports with SEC. This can make finding clients difficult.

Entrepreneurship is a great way for you to combine your accounting skills and your entrepreneurial spirit. Home-based businesses can offer you the opportunity to build a profitable business with your family's support. Although you won't have the full control of the strategic direction and management of your company, you will have the ability to concentrate on what you do best. You can help your clients with your accounting skills, even if you have a small business.

FAQ

What should I do when hiring an accountant?

Ask about their qualifications, experience, and references when interviewing an accountant.

You want someone who's done this before and who knows the ropes.

Ask them for any specific skills or knowledge that they might have that you would find helpful.

Make sure they have a good name in the community.

What is the significance of bookkeeping and accounting

Bookkeeping and accounting is essential for any business. They are essential for any business to keep track and monitor all transactions.

These items will also ensure that you don't spend too much on unnecessary items.

It is important to know the profit margin from each sale. It is also important to know how much you owe others.

You can raise your prices if you don’t have enough cash coming in. But, raising prices too high could result in customers being turned away.

You might consider selling off inventory that is larger than you actually need.

If you have less than you need, you could cut back on certain services or products.

All these things will affect your bottom line.

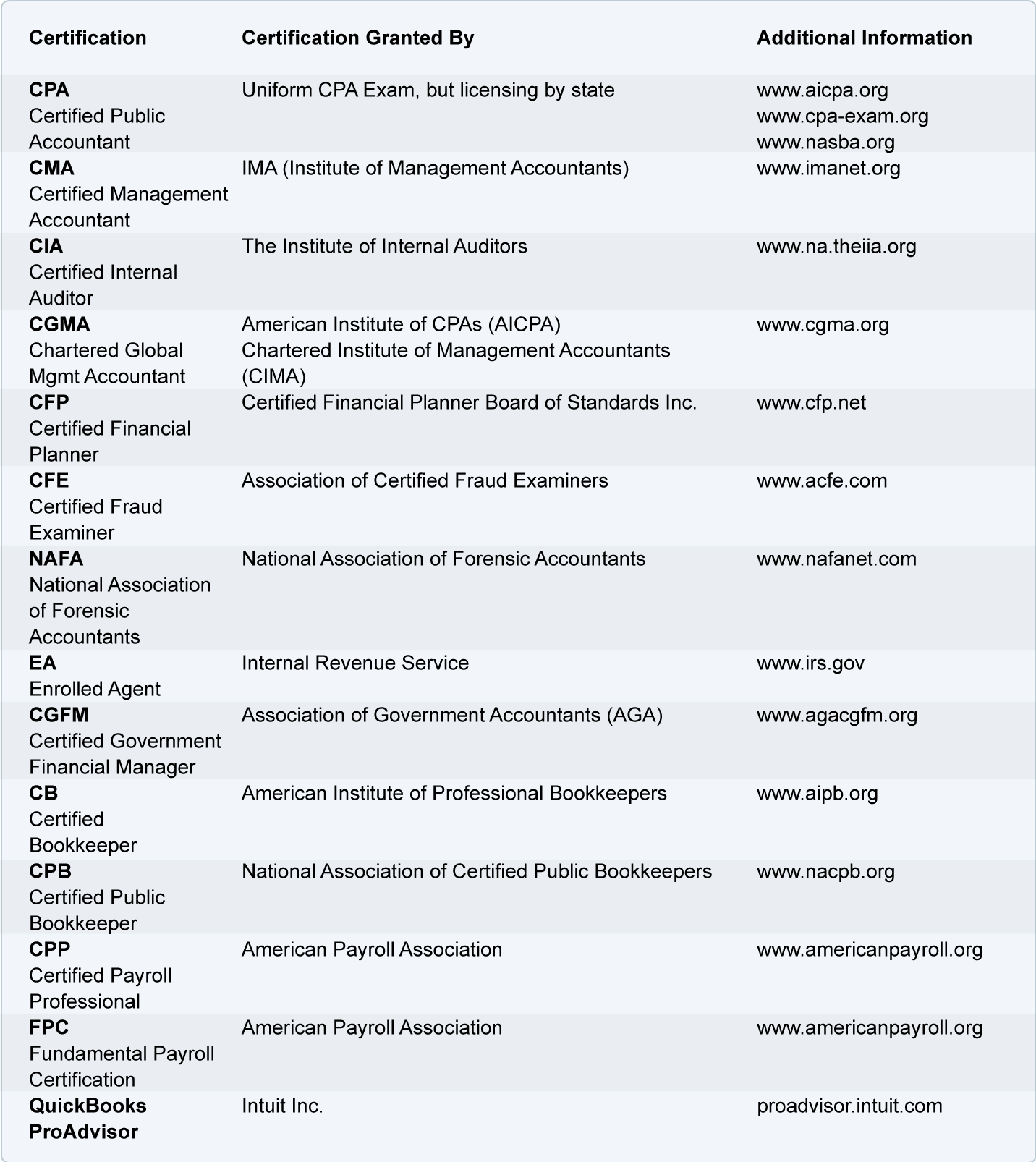

How long does it take for an accountant to become one?

Passing the CPA exam is required to become an accountant. Most people who desire to become accountants study approximately four years before they sit down for the exam.

After passing the exam, one must be an associate for at most 3 years in order to become a certified public accounting (CPA) after passing it.

What is the purpose accounting?

Accounting is a way to see a financial picture by recording, analyzing and reporting transactions between people. It enables organizations to make informed decisions regarding how much money they have available for investment, how much income they are likely to earn from operations, and whether they need to raise additional capital.

To provide information on financial activities, accountants record transactions.

This data allows the organization plan for its future business strategy.

It is important that the data you provide be accurate and reliable.

What is a Certified Public Accountant, and what does it mean?

Certified public accountant (C.P.A.). A person who is certified in public accounting (C.P.A.) has specialized knowledge in the field of accounting. He/she knows how to prepare tax returns and assist businesses in making sound business decisions.

He/She also keeps track of the company's cash flow and makes sure that the company is running smoothly.

What is the distinction between bookkeeping or accounting?

Accounting is the study and analysis of financial transactions. Bookkeeping records these transactions.

The two are related but separate activities.

Accounting deals primarily on numbers, while bookkeeping deals mostly with people.

For the purpose of reporting on financial conditions of organizations, bookkeepers maintain financial information.

They adjust entries in accounts payable, receivable, and payroll to ensure that all books are balanced.

Accountants examine financial statements in order to determine whether they conform with generally accepted accounting practices (GAAP).

They might recommend changes to GAAP, if not.

Bookkeepers keep records of financial transactions so that the data can be analyzed by accountants.

Statistics

- In fact, a TD Bank survey polled over 500 U.S. small business owners discovered that bookkeeping is their most hated, with the next most hated task falling a whopping 24% behind. (kpmgspark.com)

- Given that over 40% of people in this career field have earned a bachelor's degree, we're listing a bachelor's degree in accounting as step one so you can be competitive in the job market. (yourfreecareertest.com)

- BooksTime makes sure your numbers are 100% accurate (bookstime.com)

- Given that over 40% of people in this career field have earned a bachelor's degree, we're listing a bachelor's degree in accounting as step one so you can be competitive in the job market. (yourfreecareertest.com)

- a little over 40% of accountants have earned a bachelor's degree. (yourfreecareertest.com)

External Links

How To

Accounting for Small Business

Accounting is a critical part of running a small business. This includes tracking income and expenses, preparing financial statements, and paying taxes. Quickbooks Online is one of the software programs that can be used. There are many options for accounting small businesses. You should choose the best way for you according to your needs. Here are some top options that you can consider.

-

You can use paper accounting. If you like simplicity, paper accounting might be the best option. This method is very simple. All you need to do is keep track of all transactions. If you are looking to ensure that your records are accurate and complete, you may want to consider QuickBooks Online.

-

Online accounting is a great option. Online accounting makes it easy to access your accounts anywhere, anytime. Some popular options include Xero, Freshbooks, and Wave Systems. These software allows you to manage your finances and generate reports. They offer great features and benefits, and they are easy to use. So if you want to save time and money when it comes to accounting, you should definitely try out these programs.

-

Use cloud accounting. Cloud accounting is another option that you could use. It allows you to store your data securely on a remote server. Cloud accounting has many advantages when compared to traditional accounting software. It doesn't require you to purchase expensive hardware or software. Your information is kept remotely and offers you better security. It also saves you time and effort in backing up your data. It also makes it easier to share your files.

-

Use bookkeeping software. Bookkeeping software works in the same way as cloud accounting. However, you will need to buy a computer to install the software. After installing the software, you will be able to connect to the internet so that you can access your accounts whenever you want. You will also have the ability to access your accounts and balances directly from your PC.

-

Use spreadsheets. Spreadsheets can be used to manually enter financial transactions. A spreadsheet can be used to record sales figures for each day. Another good thing about using a spreadsheet is that you can change them whenever you want without needing to update the entire document.

-

Use a cash book. A cashbook allows you to record every transaction. There are many sizes and shapes of cashbooks, depending on the space available. You have the option of using a different notebook for each month, or a single notebook that covers several months.

-

Use a check register. You can use a check register as a tool to help you organize receipts or payments. To transfer items to your check list, all you have to do is scan them in your scanner. You can then add notes to help remember what you bought later.

-

Use a journal. A journal is a type of logbook that keeps track of your expenses. This is especially useful if you have frequent recurring expenses such rent, utilities, and insurance.

-

Use a diary. A diary is simply something you keep track of and that you can write in your own words. You can use it to keep track of your spending habits and plan your budget.