Contracts for contract accounting services should clearly define the fees and status of the bookkeeper. It should also indicate the frequency of payment. The frequency can be weekly, biweekly, monthly, quarterly, or on completion of the services. A retainer may be required in certain cases. Some contract bookkeepers charge an hourly fee.

Termination clause

The termination clause in a contract must be considered when determining how much revenue should be recognized for a given period. It is possible for revenue to be recognized in multiple periods of the same contract depending on the term of the agreement. If the duration of the agreement is short, the termination clause can be ignored.

A contract's termination clause can be used for convenience or default. A convenience clause allows the parties of a contract to end it early, usually after a period of time. These clauses are very common in funding agreements, government contracts and other types of agreements. These clauses are subject to varying accounting rules.

Limitation in scope

A bookkeeping contract typically limits the scope of services. To extend the scope of services, you will need to amend or create a new contract. These limitations are intended to protect the financial service provider and allow for the validation of the legitimacy or bookkeeping services. This clause must be clearly defined in the contract. Typically, the scope of services is one year. But, it's possible for business operations to change within a year. It is hard to predict future needs. A limited contract could be beneficial for both parties in such cases.

Unintended consequences can result from a limitation. This may make it difficult for the auditor to make an objective judgement about a company’s economic condition. Without access to key information, the auditor may not be able to draw an accurate conclusion about a firm's economic situation. An auditor might not be able complete the audit if his accounting records have been destroyed.

Limitation on costs

Both direct and indirect costs are covered by the principle of cost limitation in contract bookkeeping. Indirect costs are ongoing expenses that cease to exist after the contract ends. Generally, indirect costs can be tracked using the billing rates in effect at the end of the contract year or current billing rates. Indirect rates can be overlooked when costing incurred expenses. This can lead to problems in limitation reporting.

Contractors are required to keep track their costs and inform the contracting officer if they exceed the funding amount. Contracts may also require contractors keep track of their cost over a 60 day period or to perform a specific percentage of work. Contractors who seek lucrative contracts with federal government agencies require a contract bookkeeping program.

Limitation on liability

It is essential to have a limitation of liability clause for contract bookkeeping. Liability clauses are designed to limit liability to a set amount or a specific type of damage. The language used to limit liability is not always clear and reasonable. A professional should make sure the client signs the contract before he or she begins work.

Limitation of liability clauses, particularly when used in business to consumer contracts are not always enforceable. They should be considered separate sections in a contract and supported by valid documentation. While limitation of liability clauses can be legal in most states they must still be approved by the parties. To avoid confusion, they should also be written clearly.

Legal obligations

A contract is a legally binding agreement between a person or entity and another person. These obligations can either be written or oral. A politician may have written obligations to a constituent. But, they might also have unwritten ones to their donors. Although unwritten obligations can be difficult to prove, and they cannot be effectively regulated by the courts, they still constitute a legal obligation. Since Roman times, important contracts have been subject to strict legal enforcement by courts.

A contract bookkeeper must not only keep records but also provide information about sales. This includes reporting tax and social insurance returns and providing copies of all documents required for bookkeeping. The contract bookkeeper is also legally required to submit an annual report. It includes the preparation of a profit-and-loss account and balance sheet.

FAQ

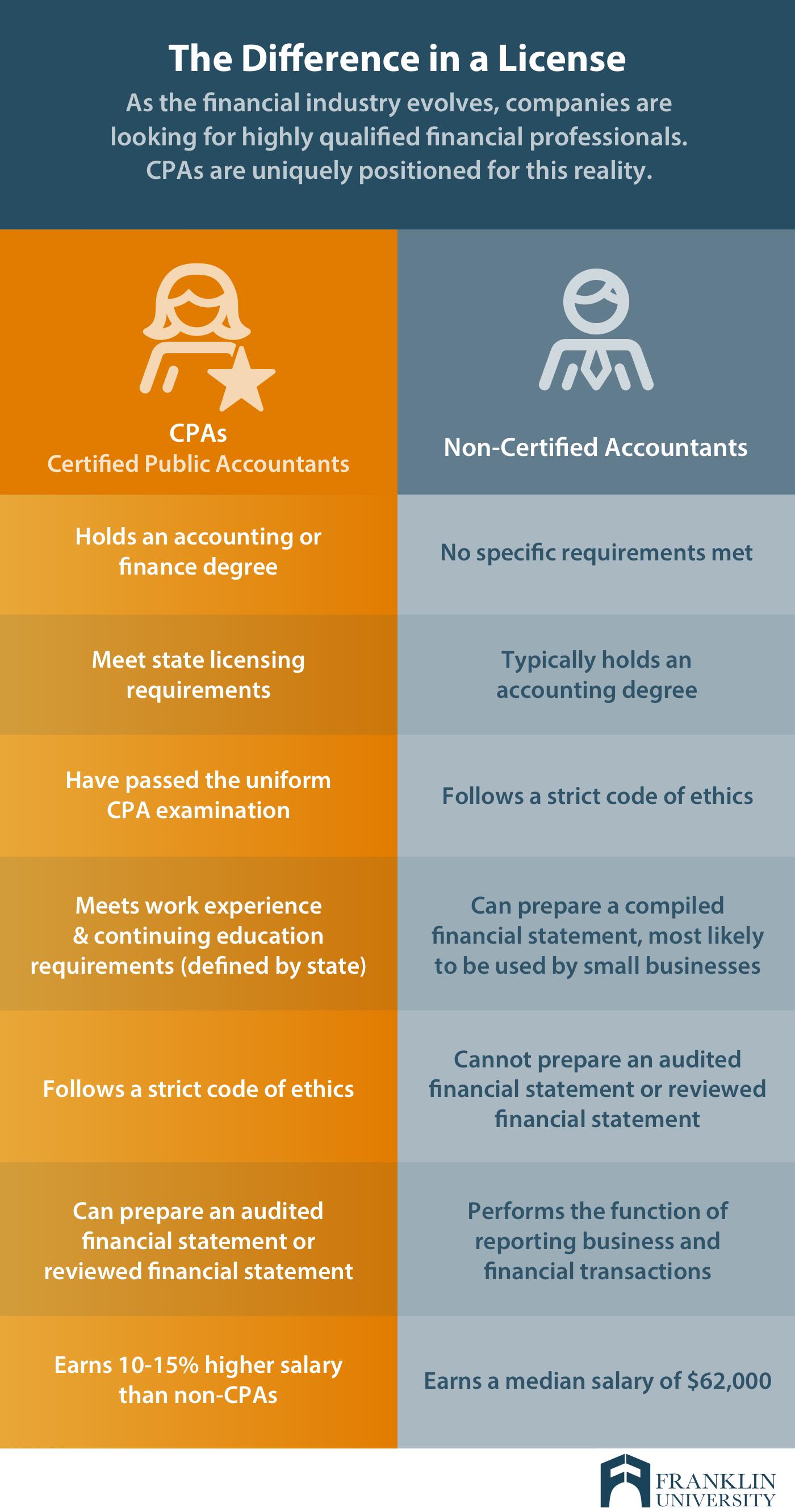

What is a Certified Public Accountant and how do they work?

Certified public accountant (C.P.A.). An accountant with specialized knowledge is one who has been certified as a public accountant (C.P.A.). He/she is able to prepare tax returns and help businesses make sound business decisions.

He/She keeps an eye on the company's cash flow, and ensures that everything runs smoothly.

What happens to my bank statement if it is not reconciled?

If you fail to reconcile your bank statement, you may not realize that you've made a mistake until after the end of the month.

At that point, you'll have to go through the entire process again.

What is the work of accountants?

Accountants work with clients to ensure they make the most out of their money.

They also work closely with professional such as attorneys, bankers or auditors.

They also interact with departments within the company, such as sales and marketing.

Accountants are responsible in ensuring that books are balanced.

They calculate the amount of tax that must be paid and collect it.

They prepare financial statements that show the company's financial performance.

What are the differences between different bookkeeping systems?

There are three types of bookkeeping systems available: computerized, manual and hybrid.

Manual bookkeeping means using pen and paper to maintain records. This method requires constant attention.

Software programs are used for computerized bookkeeping to manage finances. It is time- and labor-savings.

Hybrid Bookkeeping is a hybrid of manual and computerized methods.

What does an accountant do, and why is it so important?

An accountant keeps track all the money that you earn and spend. An accountant also records how much tax you have to pay and the deductions that are allowed.

Accounting helps you manage your finances by keeping track your income and expenses.

They are responsible for preparing financial reports that can be used by individuals or businesses.

Accountants are essential because they need to understand everything about numbers.

A professional accountant can also help with taxes, so that people pay as little tax as they possibly can.

What is an audit?

An audit is a review or examination of financial statements. Auditors examine the company's books to verify everything is correct.

Auditors look for discrepancies between what was reported and what actually happened.

They also examine whether financial statements for the company have been properly prepared.

Statistics

- In fact, a TD Bank survey polled over 500 U.S. small business owners discovered that bookkeeping is their most hated, with the next most hated task falling a whopping 24% behind. (kpmgspark.com)

- According to the BLS, accounting and auditing professionals reported a 2020 median annual salary of $73,560, which is nearly double that of the national average earnings for all workers.1 (rasmussen.edu)

- BooksTime makes sure your numbers are 100% accurate (bookstime.com)

- Given that over 40% of people in this career field have earned a bachelor's degree, we're listing a bachelor's degree in accounting as step one so you can be competitive in the job market. (yourfreecareertest.com)

- Given that over 40% of people in this career field have earned a bachelor's degree, we're listing a bachelor's degree in accounting as step one so you can be competitive in the job market. (yourfreecareertest.com)

External Links

How To

How to become an accountant

Accounting is the science behind recording transactions and analysing financial data. Accounting can also include the preparation of reports or statements for various purposes.

A Certified Public Accountant or CPA is someone who has passed an exam and received a license from the state board.

An Accredited financial analyst (AFA), or an individual who meets the requirements of the American Association of Individual Investors, is an individual who is accredited by Financial Analysts. A minimum five-year investment history is required in order to be an AFA according to the AAII. They must pass a series of examinations designed to test their knowledge of accounting principles and securities analysis.

A Chartered Professional Accountant (CPA), sometimes referred to as a chartered accountant, is a professional accountant who has been awarded a degree from a recognized university. CPAs must meet specific educational standards established by the Institute of Chartered Accountants of England & Wales (ICAEW).

A Certified Management Accountant is a professional accountant who specializes in management accounting. CMAs must pass exams administered annually by the ICAEW. They also need to continue continuing education throughout their careers.

A Certified General Accountant is a member of American Institute of Certified Public Accountants. CGAs must take multiple tests. One of these is the Uniform Certification Examination (UCE).

A Certified Information Systems Auditor (CIA) is a certification offered by the International Society of Cost Estimators (ISCES). Candidates for the CIA certification must complete three levels, which include coursework, practical training and a final assessment.

Accredited Corporate Compliance Official (ACCO), a title granted by ACCO Foundation and International Organization of Securities Commissions. ACOs must hold a baccalaureate or higher degree in business administration, finance, or public policy. Additionally, they must pass two written and one verbal exams.

The National Association of State Boards of Accountancy offers the certification of Certified Fraud Examiners (CFE). Candidates must pass three exams and obtain a minimum score of 70 percent.

International Federation of Accountants is accredited a Certified Internal Audior (CIA). Candidates must pass four exams covering topics such as auditing, risk assessment, fraud prevention, ethics, and compliance.

American Academy of Forensic Sciences gives Associate in Forensic Accounting (AFE), a designation. AFEs must have graduated with a bachelor’s degree from an approved college or university in any other study area than accounting.

What does an auditor do? Auditors are professionals who conduct audits of organizations' internal controls over financial reporting. Audits can either be done randomly or based on complaints about financial statements received by regulators.